7. Conclusion and Recommendation

Two hypotheses designed to achieve the research objective were tested and discussed under the research findings. Field research data have been collected and relevant output analysed.

This chapter draws conclusions and recommends a future best practice template that supports business managers to be more successful in strategy selection and implementation.

During the discussion references to the literature review in part 2 are made.

7.1 Conclusion on Research

Research questions formed the basis for a field survey, and the data output was analysed and discussed in research findings to test the validity of two hypotheses.

7.1.1 Strategy Development and Selection

The hypothesis to be tested was:

(1) Vision, mission and strategic intent is heavily influenced by the competitive forces and motives in the sense making process.

International companies were found to be influenced differently when addressing environmental objectives. Global trends offer both threats and opportunities and thus influence differently on “perceived future” among international companies when compared to local companies.

It was evident in the analysis of competitive environment and position in value network that businesses did not have a shared knowledge of future environmental opportunities and threats.

The difference in perceptions of future challenges was also evident in how the challenges influenced environmental objectives. Stakeholder objectives were adapted towards the difference in opportunities and threats according to level of internationalisation and position in the value network.

Generic competitive strategies did not influence the strategic intent, but this could be industry specific.

The competence level did not have an evident influence on strategic intent, and this could stem from a national competitive advantage, based on high environmental threshold levels and thus culture and competencies in the industry.

Cooperative and competitive motives were seen to influence the strategic intent and determinants of business profitability or philanthropic motives.

The overall tendency is that strategic intent is influenced by the ability to see the company benefits, but might be influenced by functional cultural attitudes or “how we perceive the world” and “how we see ourselves in the world”.

It is important to remember that strategic objectives are not created by business, but by managers (Macover, 1994 p22), and that this research measure manager’s perceptions.

Personal perceptions are thus influenced by internationalisation, position in the industry and functional position in own organisation, and thus influence the selection of strategic environmental objectives.

Global trends and difference in stakeholder power influence the future challenges.

Human perception and behaviour influence the present environmental business objectives.

The hypothesis is confirmed. There was only one research question not confirming the hypothesis.

Based on the differences in the perceived future and present challenges in the value network, a risk for unsustainable (loose-loose) value creation in the indu-stry seems indicated (Laszlo, 2005 p126; illustrated in figure 11).

This could be a major challenge to the Danish concrete industry. To minimize this risk it appears that to support business managers to be more successful in strategy development and selection, the competitive and cooperative motives are the most important area to improve.

7.1.2 Strategy Implementation

The hypothesis to be tested was:

(2) Outcomes of strategic intent are heavily influenced by allocation of investments, resources and performance management practice.

There were a relative high number of respondents (59%) that stated a need for a tool box.

From the analysis there was no clear connection between environmental outcomes and the “need of ease” for putting up a business plan and implementing environmental initiatives, nor the Key Success Factors in the industry.

It was well documented that despite differences in “strategic focus” the outcomes were unchanged, and when comparing outcomes to “strategic objectives” initiatives regarding product development and branding were unchanged.

Follow up and reporting showed strong relationship to achievement of a high level of outcomes, without regards to what type of reporting that was used.

The overall tendency is that outcomes of strategic intent are more related to performance management practices than to the strategic intent. This means that “what you get is – what you measure” and not “- what your objective and focus is”. Also timing differences in historically intended objectives versus the measurements of today, influence the human perception of what is important tomorrow.

In respect of this, it is important to remember that alignment of business objectives to business policies and practices and measurement of organisational progress is a business management responsibility.

Tomorrow you will get what you measure today not what your intention was yesterday

The hypothesis is partially confirmed. Performance management practices influence outcomes of strategic intent, whereas allocation of investments and resources were not adequately determined in the field analysis.

Reflecting on the sentence of Laszlo (2005 p31) “what gets measured gets managed” it can be concluded on the basis of the analysis that, to support managers to be more successful in strategy implementation the most important area improve is the alignment of strategic objectives with measured outcomes.

7.2 Recommendation for Future Business practice

To recommend a future best practice template that supports business mana-gers to be more successful in strategy selection and implementation, Laszlo’s Eight Disciplines (Laszlo, 2005 p122) are used as a framework for strategy development, selection and implementation.

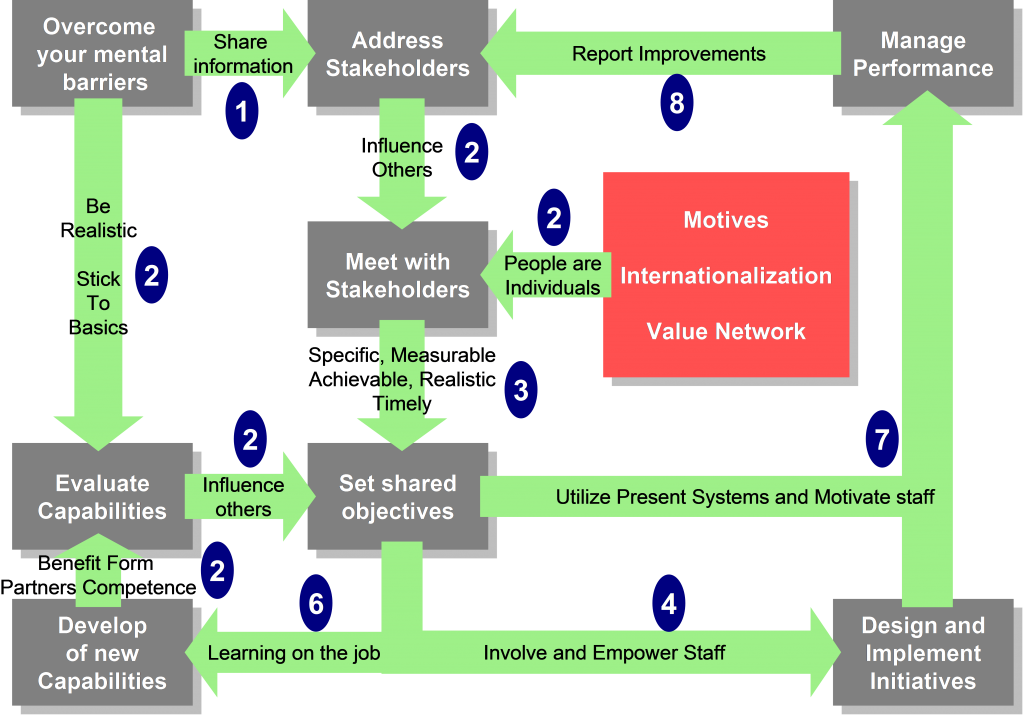

Figure 18 describes the recommended path to stakeholder alignment with reference to seven of Laszlo’s disciplines. The last discipline will be presented in more detail under 7.2.2 “5) Develop the Business Case”.

Figure 18: CSR Stakeholder Alignment Path

Source: Author’s own creation based on reviewed literature

A detailed best practice template describing guidelines for securing stakeholder alignment in the Danish concrete industry is presented in appendix 7.

7.2.1 Strategy Development and Selection

Based on the research results a best practice template suggests how to secure a balance of competitive and cooperative motives. The purpose is to support managers in a change process and assist them in more successful environmental strategy development and selection.

1) Understand current position

To understand how the company best creates or destroys stakeholder value the best practice would be to initiate customer and supplier dialogue.

The “Shareholder/Stakeholder Map” (Laszlo, 2005 p126), illustrated in figure 11, can be used to map the identified areas for potential improvements. Mapping of shareholder value demands for financial insight and determination of method. The “Value Drivers” (Laszlo, 2005 p151) is an easy to use and understand guideline in the basis for assessment.

Managers will benefit from knowledge regarding present customer needs and supplier capabilities, which will enable them to increase shareholder value.

The manager’s risk in changing cooperative level and sharing knowledge is small, as 91% of industry managers include others in the value network as important stakeholders in vision and mission.

2) Anticipate future expectations

To see the full picture of tomorrow the best practice is to receive information from your industry body, as they follow trends related to the industry.

The “Generations, Business Context and CSR labels” figure 4 can be used to understand the increasing rate in which society is changing, and the text in 2.1.1 to 2.1.3 illustrate the complexity in understanding causes and effects in society. Laszlo (2005 p136) also provides a good framework for the key-steps in scenario building.

Managers will benefit from this by saving time on guesses themselves, and to receive knowledge with a higher level of credibility, reliability and validity as it is based on objective research and analysis. Relating to mainstream practices relevant to the industry is also emphasised as important in literature (Kotler & Lee, 2005), and industry shared knowledge will support managers in achieving a shared perception of future challenges.

The risk of basing business on industry knowledge is small and lover than making own guesses.

Makover (1994 p28) states that ”No profession can really develop which does not have an intellectual content shaped broadly by many men, and this condition does not yet exist in business.” This was originally stated in 1927 by Wallace B. Donham in the article “The Social Significance of Business”, Harvard Business Review.

3) Set sustainable values and goals

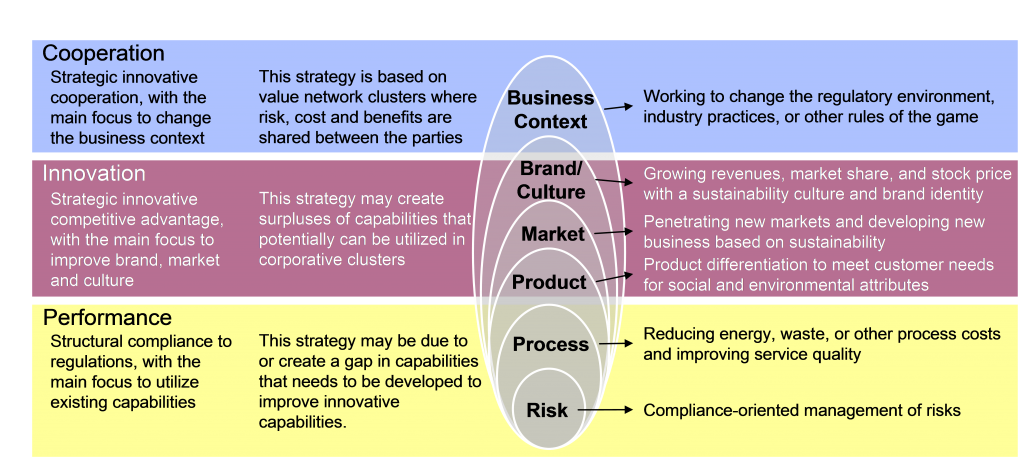

To manage stakeholder satisfaction well the objectives must be related to “A Firms Stakeholders” (Werther & Chandler, 2006 p4) in figure 7. Defining and communicating environmental objectives that are specific, measurable, acceptable and timely is needed to follow up correctly. Suitability, feasibility and acceptability can be secured by addressing the identified issues from the stakeholder conversations under point 1.

Grouping the objectives into the CSR strategy categories below, allows dialogue concerning capabilities needed and the outcomes that are to be followed up (figure 19).

Figure 19: CSR Strategy Grouping and Checklist

Source: Author’s own creation based on Laszlo (2005)

Managers will benefit from a lower level of resistance when engaging in environmental objectives, as they can relate objectives to stakeholder needs with well formulated goals and outcomes, with clear defined strategies and refer to utilization of business capabilities.

There are no risk in securing well defined objectives and goals related to stakeholder needs and formulating strategies for how to achieve these goals based on the company’s capabilities. The risk if not doing it is that the organisations do not know what to do when and why.

One important issue is to remember to address business profitability, in goals and in expected outcomes. If not doing so, stakeholders might suspect there is a “hidden agenda” as nobody expects a business to be purely philanthropic. Better be honest than loose stakeholder thrust and cooperation.

4) Design value creating initiatives

One of the important issues determined in the literature review is to engage employees in designing and creating the environmental initiatives.

The organisation can assist in determination of which environmental capabilities (competence and resources) that are available in or outside the organisation.

The “Assessing the Target Zone for Capabilities” (Laszlo, 2005 p149) framework in figure 14 is useful in capability assessment. The model for “Assessing the Target Zone for Capabilities” assist in identifying the capability surpluses and gaps, by mapping current performance against importance of the needed capabilities, and lead to a prioritized set of initiatives that lead the corporation towards the sustainable value (win-win) quadrant illustrated in figure 11.

The “CSR Strategy Grouping and Checklist” figure and the “six CSR initiatives” (Laszlo, 2005) can assist in creation of the initiatives (figure 19).

Kotler & Lee (2005 p53-179) describe and illustrate by cases a framework of six CSR initiatives that are to be managed by deliberate strategic decisions. The strategic decisions are to align the CSR initiatives to business values, objectives, products, markets and brands.

Managers will benefit later on of higher employee commitment and have overcome barriers of change in the organisation. The needed to win capabilities that have been defined in the process, can be seen as key source of competitive advantage, with a clear distinction from competitors, and thus provide higher returns through excellent performance.

The risk of involving employees is waste of time, if objectives and strategic direction (performance, innovation and partnership) is not determined beforehand.

7.2.2 Strategy Implementation

Based on the research results a best practice template suggests how managers can improve alignment of environmental strategic objectives with measured outcomes.

5) Develop the business case

Based on this analysis the strategic objectives (or call it motivation) for selecting strategies are mostly based on stakeholder satisfaction and determined to be linked to economic stakeholders such as customers, suppliers and creditors.

It would be easier for managers to put up a business plan for environmental improvements, if they know the stakeholder motives and how they can overcome their resistance. Having thought this out the best thing to do is to get stakeholder commitment and acceptance to the objective by meeting stakeholder needs. This seems simple, but is difficult in practice.

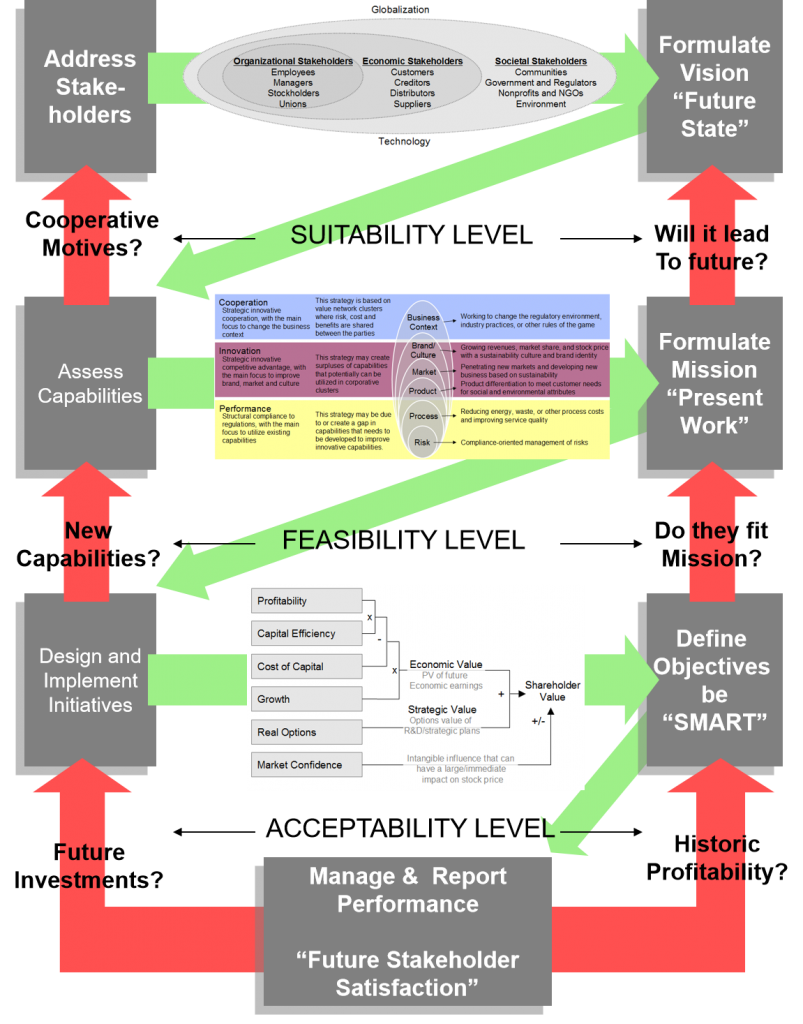

Figure 20 describes the recommended path for more successful creation of business cases promoting environmental improvement, with reference to four steps below that is seen to improve suitability, feasibility and acceptability.

STEP I

Managers can map their stakeholders (“A Firms Stakeholders”, Werther & Chandler, 2006 p4) and determine their motives (“Shareholder/Stakeholder Map”, Laszlo, 2005 p126). Hereafter the different stakeholder needs can be put together and form the strategic environmental objectives.

Figure 20: CSR Business Case Alignment Path

Source: Author’s own creation based on reviewed literature

STEP II

The “CSR Strategy Grouping and Checklist” figure 19 and the “six CSR initiatives” (Kotler & Lee, 2005) can assist in presentation of the strategic objective, and be used to argument the strategic fit to the general business strategies.

One of the prerequisite capabilities in promoting environmental improvements, are the ability to describe the potential negative consequences if not acting environmental responsible in a well augmented way. The extensive CSR literature could assist in promoting the “six CSR initiatives” (figure 19), but the Performance related arguments in “Risk” and “Process” improvements will be the easiest to valuate and argue. Penalties and fines for not complying legal issues or regulations are seen as the major driver of CSR initiatives.

STEP III

The strategic objectives can then be linked to the “Real Options” section in the “Value Drivers” (Laszlo, 2005 p151) and form the financial argument in the business plan. The financial figures are best to be presented using the preferred way of calculation in the business (NPV or IRR). Involvement of financial specialists is preferable to secure the quality of calculations according to business accounting principles and internal organisational support.

Engaging and empowering employees to act and to benefit from quick-wins can be considered as an alternative route to setting up business plans, and may lead to a long-term sustainable environmental culture in the organisation.

A practical case story and a simple business case example are presented in appendix 8 and 9.

STEP IV

The recommended SFA-analysis in appendix 10 is to support manager’s ability to successfully promote and implement environmental improvements. It is Important to follow up on performance, as reporting of historic profitability on environmental investments, will lead to less future stakeholder resistance.

Managers will benefit from the ability to promote a simple business plan that is both financial well formulated and strategic aligned to stakeholder expectations. If addressing the “Performance” related initiatives (figure 19) they would also experience that the business profitability arguments are easier to promote.

The risks involved in setting up a business plan for environmental improvements will be considerably reduced if suitability, feasibility and acceptability is reviewed.

6) Capture the value

Important issues relevant to this recommendation are to prioritize environmental issues and to implement simple ethical policies or guidelines that support employees in prioritisation of time and day-to-day decision making.

This is supported by Hopkins (2003) who sees commitment in caring in stakeholders and the environment to be encompassed by good ethics, both within the wall and without.

Acknowledgement of ethics as the core in management decisions and policies is requested by Frederick (2006 p90). He recommends that corporations should employ and train managers, align policies, core values and culture to ethics and detect and correct wrong behaviours.

7) Validate results and capture learning

Implementation of continuous measurement in the present quality, performance management systems and annual reports are primary driver in achieving results.

Just aiming at and documenting that the Danish threshold levels are achieved could be sufficient as the level is well above international standards.

8) Build sustainable value capacity

This point consists of continuous learning and improvement of systems, pro-cesses, initiatives and competences (Laszlo 2005 p158).

The ultimate objective is alignment of culture and brand described by Kunde (1997) and Kotler & Keller (2006 p174) both highlighting the importance of corporations fully connecting with the customers and the alignment of identity and relationship in the “Brand Resonance Pyramid” (Kotler & Keller, 2006 p281).

7.3 Limitations of the Research

As stated in 4.3.1 there are limitations in the reliability, validity and generalisability of the research results. The response rate could have been increased if the time and resources were available for the research.

To achieve a true and valid representative data output, the sampling strategy could have been based on either random or cluster sampling. Again due to limitations and regulations in access to contact data this was not possible.

The research method could have been improved by combining the quantitative survey with qualitative analysis. This would have increased the credibility and usability especially in the conclusion and recommendation part.

A qualitative method would also have been able to facilitate an exploration of the more soft factors in the sense making process, and perhaps describe the different mental models and motives in the industry.

The size of businesses would have been appropriate to include in the research. This could have enabled an analysis of different sense making processes in small and large businesses.

Principles for allocation of investments and resources turned out to be almost impossible to analyse based on a quantitative research method, and would perhaps be an area that could benefit by a qualitative analysis.

The moving target and undefined context of CSR is also a limitation to the research. Difference in perception and interpretation of words are likely to have influenced the output, despite the work put into translation and qualitative interviews in the process of questionnaire formulation.

As the research builds on existing theory it does not bring any new evidence or theoretical explanations. Thus it is seen as unlikely that there have been any new discoveries of benefit to the academic community. Some of the existing theory was confirmed, and other theories tested were not confirmable, but this could be industry specific.

Further qualitative research regarding the co-operative and competitive motives in the industry could assist in description in how best to overcome own personal beliefs and create shared win-win outcomes.